If you read every published report on Indian EV infrastructure from the last 24 months, you would walk away believing that the country's electrification story is happening in seven cities: Bangalore, Mumbai, Delhi NCR, Hyderabad, Pune, Chennai, and Kolkata.

You would be wrong by an order of magnitude.

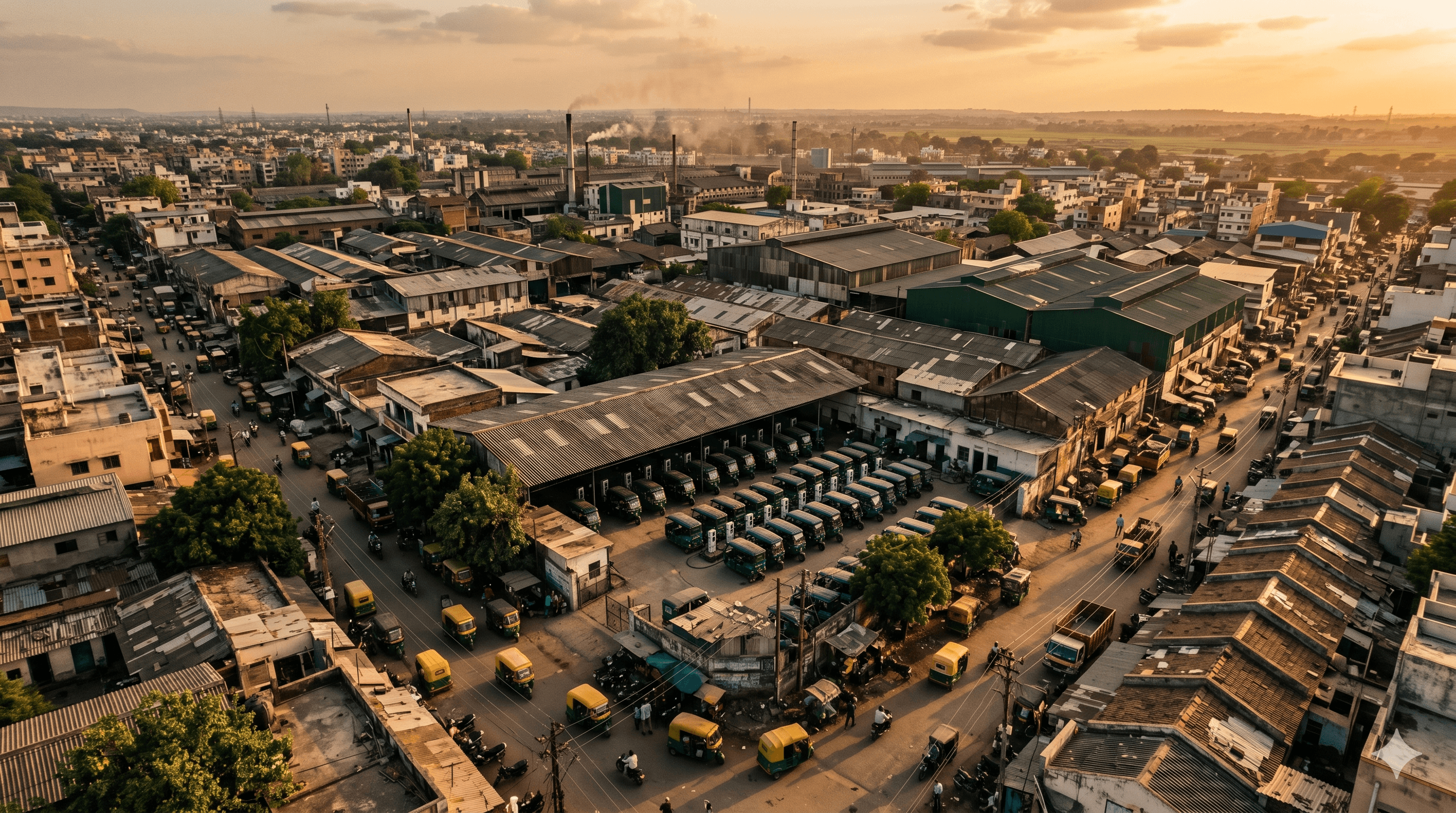

The fastest-growing pockets of EV adoption in India today are not in the metros. They are in the industrial clusters of Tier 2 cities — places where the press doesn't have offices, where ribbon-cutting events don't get covered, and where fleet operators are quietly making conversion decisions on spreadsheet logic that has nothing to do with climate optics.

This is the side of the Indian EV story that almost no one is mapping. So we're going to start mapping it.

Why Tier 2 is winning the fleet electrification race

There's a simple economic reason Tier 2 industrial clusters are leading commercial EV adoption.

Operators in metros have higher gross margins, cheaper financing, larger fleets, and more diversified revenue. The pain of high fuel cost is real but absorbable. Operators in Tier 2 industrial clusters — three-wheeler fleets in Coimbatore, intra-city logistics in Surat, last-mile delivery in Indore, contract transport in Vizag — operate in single-digit-percent gross-margin businesses where the difference between ₹3.5/km in fuel cost and ₹0.9/km in electricity is not a marginal improvement. It is the difference between making payroll and not.

The economics of conversion are stark:

- A petrol-CNG 3-wheeler in Coimbatore burns roughly ₹2.5–3.5 per km in fuel.

- An equivalent electric 3-wheeler with depot charging or swap burns ₹0.7–1.2 per km in equivalent energy cost.

- Maintenance costs drop by another ₹0.2–0.5 per km.

- For a vehicle that runs 150–200 km/day, the gross saving is ₹500–1,000 per vehicle per day.

- For a 100-vehicle fleet, that is ₹50,000–₹1,00,000 per day, or ₹1.5–3 Cr per year, before counting financing math.

This isn't theoretical. This is happening today, vehicle by vehicle, depot by depot, across half a dozen Tier 2 clusters. The conversion is being financed by NBFCs, OEM-captive lenders, and increasingly, fintech partnerships designed specifically for fleet electrification. The infrastructure to support it is being built privately, behind compound walls, on negotiated tariffs, with utilization rates that public charging networks can only dream about.

Data illustration · EV-P2

Fleet Running Cost: CNG/Petrol vs. Electric 3-Wheeler

Tier 2 market conditions (Coimbatore-equivalent) · per km operated

CNG / Petrol 3-Wheeler

₹3.0 / km avg (range ₹2.5–3.5)

Electric 3-Wheeler (Depot / Swap)

₹0.9 / km avg (range ₹0.7–1.2)

Includes fuel/energy cost only. EV maintenance savings (₹0.2–0.5/km additional) not shown.

What this means for a fleet operator

Saving per vehicle / day

₹500–1,000

at 150–200 km / day

100-vehicle fleet / day

₹50K–1L

in direct fuel savings

Same fleet, annually

₹1.5–3 Cr

before financing adjustments

Operator conversations and field estimates · Prime Bottomline Ventures research · May 2026

Eight clusters worth knowing

Here's a starter map. Not exhaustive, but representative of where the fleet-led EV story is most advanced.

Coimbatore (Tamil Nadu). India's textile and auto-component capital. PSG Tech and Coimbatore Institute of Technology produce a steady stream of mechanical and electrical engineering talent. Three-wheeler fleet operators in the city have been among the earliest movers; multiple battery swap stations are operational. State EV policy (Tamil Nadu's 2023 framework) is one of the most operator-friendly in the country. This is also Prime Bottomline Ventures' home base — and the city we expect to surface the most under-publicized EV operating businesses from.

Surat (Gujarat). Diamond and textile capital of India. Massive intra-city logistics and contract-transport demand. Surat Municipal Corporation has been aggressive on EV-only zones and public charging tenders, but the more interesting story is the private fleet conversion happening across the textile-cluster ecosystem. Gujarat's EV policy framework, while less famous than Maharashtra's, is quietly competitive.

Indore (Madhya Pradesh). Smart City designation, robust intra-state logistics, growing 3-wheeler EV penetration. Indore is the lead Tier 2 city for several national fleet operators because of its central geography and supportive municipal posture.

Vizag (Andhra Pradesh). Port city with significant industrial backbone (steel, pharma, chemicals). Andhra Pradesh's EV policy has been investor-friendly. Vizag's commercial fleet base — particularly intra-city goods movement — is electrifying faster than most outsiders realize.

Jaipur (Rajasthan). Tourism and commerce hub with strong 2-wheeler density and tourism-driven 3-wheeler demand. Rajasthan EV Policy 2022 created a window for private operators that several have moved into.

Madurai and Tiruchirappalli (Tamil Nadu). Secondary Tamil Nadu industrial centers benefiting from the state's EV framework. Smaller volumes than Coimbatore, but increasingly interesting as the ecosystem matures.

Kochi (Kerala). Strong public-transport orientation, KSRTC EV bus fleet at scale, and growing private intra-city fleet adoption. Kerala Startup Mission has been one of the more credible state-level enablers.

Nashik (Maharashtra). Industrial cluster with auto-component density — a node in the broader Pune–Aurangabad–Nashik corridor. Smaller than the metros it sits between, but with operating economics that increasingly favor it as a depot location.

This is not a complete list. It's a starting point. Almost every one of these cities has a dozen-plus fleet operators, a handful of swap network franchisees, a small number of CPO entrepreneurs, and an even smaller number of software/middleware founders. The aggregate economic activity across these eight clusters in EV operations is meaningfully large. The aggregate press coverage of it is close to zero.

Starter map · EV-P2

8 Tier 2 Clusters with Active Fleet EV Conversion

Not exhaustive · field research and operator conversations · Prime Bottomline Ventures · May 2026

Coimbatore

HQTamil Nadu

Textiles · Auto components

Our home base · earliest 3W movers

Surat

Gujarat

Diamonds · Textiles

Aggressive EV-only zones · private fleet conversion

Indore

Madhya Pradesh

Intra-state logistics

Smart City · central geography

Vizag

Andhra Pradesh

Steel · Pharma · Port

Fast intra-city goods fleet conversion

Jaipur

Rajasthan

Tourism · Commerce

Strong 3W density · Raj EV Policy 2022

Madurai / Trichy

Tamil Nadu

Secondary industrial

Maturing ecosystem under TN framework

Kochi

Kerala

Public transit hub

KSRTC EV bus fleet at scale

Nashik

Maharashtra

Auto components

Pune–Nashik corridor depot advantage

Field visits ongoing in Coimbatore and Surat · More clusters to be added as research progresses

What this changes about how to think about the sector

Three implications.

First, the customer for Indian EV infrastructure is increasingly a Tier 2 fleet operator, not a metro private vehicle owner. Charging products designed for the latter — public AC chargers in mall parking lots, slow chargers in residential complexes, app-based metro discovery — are solving the wrong problem. The customer who actually pays full economic price, runs at high utilization, and renews their charging or swap contract is the operator who runs ten three-wheelers out of a depot in Sitra Industrial Estate in Coimbatore. Build for that customer.

Second, the geographic capital allocation in Indian EV infra is upside down. Most VC dollars deployed into Indian EV infra in 2024–25 went to companies headquartered in Bangalore, Delhi NCR, and Mumbai. Most of the unit-economic activity is happening 800 kilometres from any of those cities. There is no necessary contradiction — you can run a fleet operation in Coimbatore from a Bangalore HQ — but there is a meaningful disconnect between where the capital is and where the action is. Founders willing to be physically present in Tier 2 (because their customers are) have an underrated advantage.

Third, the talent map matters more than people realize. Coimbatore, Surat, Indore, and Vizag are not talent deserts. They have engineering colleges, they have a base of mechanical/electrical talent feeding manufacturing industries, they have ex-DISCOM and ex-OEM operators with grey hair and deep operational knowledge, and they increasingly have small founder communities. The 'we can't find people' excuse for not basing operations in Tier 2 is wearing thinner each year. The OEMs — Tata Motors, Ashok Leyland, M&M, Tata Elxsi, Bosch India — have been quietly distributing technical operations across these cities for a decade.

The flag we're planting

Prime Bottomline Ventures is headquartered in Coimbatore by deliberate choice. We believe the most under-priced opportunity in Indian early-stage venture is the revenue-stage business operating in Tier 2 India — and EV infrastructure is one of the clearest examples.

Over the next six weeks, we'll be on the ground at fleet depots in Coimbatore and Surat. We'll be talking to operators most VC press has never named. We'll be publishing what we find. Some of it will be uncomfortable. Some of it will conflict with what's been said publicly about the sector by larger funds, government bodies, and the operators themselves. We'll publish anyway, because the story isn't getting told and the founders building these businesses deserve a public articulation of what they're actually doing.

If you operate an EV fleet, charging network, swap business, or supporting software business in any of the eight clusters above — or in another Tier 2 city we haven't named — we want to hear from you.

The bottom line

- The fastest-growing EV adoption in India is in Tier 2 industrial clusters, not metros.

- The economic driver is fuel cost as a share of operator margin, not climate optics or subsidy capture.

- Capital allocation, content production, and talent attention are all geographically misaligned with where the action is.

What we're watching

- Fleet conversion data from the eight clusters above through FY27

- State-level EV policy enforcement (TN, GJ, MH, AP, KL) and how operators are actually using these frameworks

- Where the next 3–5 underpublicized Tier 2 operators emerge from

What could prove us wrong

- A metro-led private 4W EV adoption breakout that shifts the centre of gravity back to urban consumer markets

- Aggressive consolidation by national CPOs that re-centralizes the operating economics

- State policy reversals in any of the lead Tier 2 states that disrupt operator economics